| User Roles | ✗Pulse user |

The Financial Reporting Council (FRC) has recently completed its multi-year periodic review of UK and Republic of Ireland accounting standards. These updates represent the most significant shift in financial reporting since the introduction of FRS 102. The changes are designed to bring UK GAAP into closer alignment with international financial reporting standards, ensuring that accounts remain relevant and transparent for all stakeholders.

Table of contents

Key Effective Dates

It is important to recognise that the changes do not all take effect at the same time. You should prepare for two distinct implementation phases:

- Supplier Finance Arrangements: These rules apply to accounting periods beginning on or after 1 January 2025.

- The Main Periodic Review (Leases and Revenue): Most other changes, including the new lease and revenue models, apply to accounting periods beginning on or after 1 January 2026.

For example, a client with a 31 March year-end won't hit the main changes until their March 2027 accounts. This transition period ensures that you have plenty of time to familiarise yourself with the new requirements and prepare your clients accordingly.

Early adoption is permitted for the 2024 Periodic Review changes, provided that all amendments are applied at the same time.

Automatic Application and Early Adoption

- The updated standards will automatically apply within Silverfin for all accounting periods starting on or after 1 January 2026. No manual action is required for these periods as the platform will default to the new requirements.

- Silverfin also provides the flexibility to adopt these changes before the mandatory deadline. If you decide that early adoption is appropriate for a specific client, you can enable this functionality directly within the platform.

- To activate the new standards early, navigate to the Accounts Workflow for the relevant period. From there, access the General Settings template and locate the toggle for Early Adoption.

Transition

When moving to the new rules on 1 January 2026, you do not necessarily have to rewrite your 2025 accounts. Re-calculating years of old leases or complex revenue contracts is a significant task, so the FRC is offering a simplified transition option to save accountants from the burden of full retrospective restatement. This choice is available to all entities reporting under FRS 102, FRS 102 Section 1A, and FRS 105.

Within Silverfin, you can choose between a Full Retrospective approach and a Simplified approach.

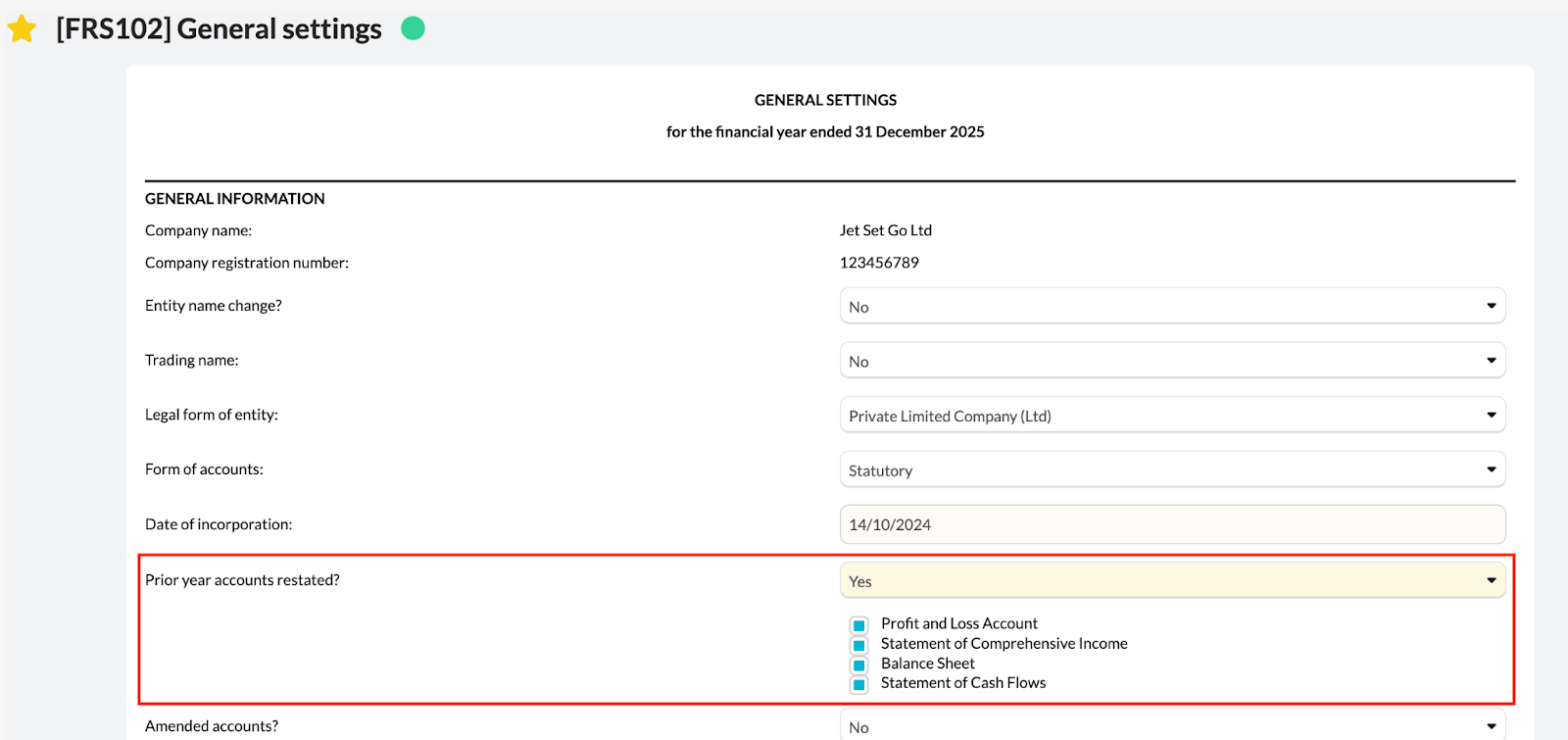

- The Full Retrospective method involves restating every figure in your accounts as if the new rules had always existed. To do this, you will need to navigate to the Accounts Workflow for the relevant period. From there, access the General Settings template and locate the toggle for Prior year accounts restated?. This then allows you to toggle which statements have been restated. See the screenshot below.

- The Simplified method allows you to keep the 2025 comparative figures as they are and instead put any necessary adjustments through the opening reserves on 1 January 2026. To do this, you will simply need to create a journal adjustment.

Who is Affected?

These updates impact all entities reporting under FRS 102 and FRS 105. For those using FRS102 Section 1A, the review introduces several new mandatory disclosures that were previously only encouraged. Silverfin users should begin assessing their client portfolios now to identify those with significant lease commitments or complex revenue contracts.

Headlines & Key Changes

1. The Lease Revolution: Bringing Leases On-Balance Sheet

- The Change: Almost all leases, including office rent and vehicles, must now be recorded on the balance sheet. The old distinction between "operating" and "finance" leases has been removed for lessees. Exemptions from these changes remain for leases with a term of 12 months or less and leases of low-value assets.

- Context: Previously, many leases were "off-balance sheet," meaning the full liability wasn't visible. The FRC is aligning FRS 102 with international standards (IFRS 16) so that a company's financial position more accurately reflects its long-term lease commitments.

- Applicable Frameworks: This change applies to FRS 102 and FRS 102 Section 1A. It does not currently apply to micro-entities reporting under FRS 105, which will continue to account for leases as an expense.

- Silverfin Impact: You will now need to recognise a Right-of-Use (ROU) Asset and a corresponding Lease Liability for nearly every lease. To support this, new working papers and accounts templates have been added to Silverfin to automate the calculation for the initial recognition of these assets, as well as the ongoing year on year interest and depreciation. These templates ensure that the correct balances flow directly into your financial statements while maintaining clear documentation of all lease judgements. Please follow the link to our dedicated help article for full information on the new Lease Liabilities and Right of Use Assets updates in Silverfin.

2. Revenue Recognition: The Move to the Five-Step Model

- The Change: Revenue can no longer be recognised based on a simple transfer of risks and rewards. Instead, you must follow the five-step process to decide exactly when and how much revenue to record.

- Context: The old rules could be interpreted in different ways, leading to inconsistency. This new framework (based on IFRS 15) ensures that revenue is only recognised when a company has actually "delivered" on the specific promises made to a customer.

- Applicable Frameworks: This change applies to FRS 102, FRS 102 Section 1A, and FRS 105. All reporting entities must adopt the new five-step model, though the level of required disclosure will vary.

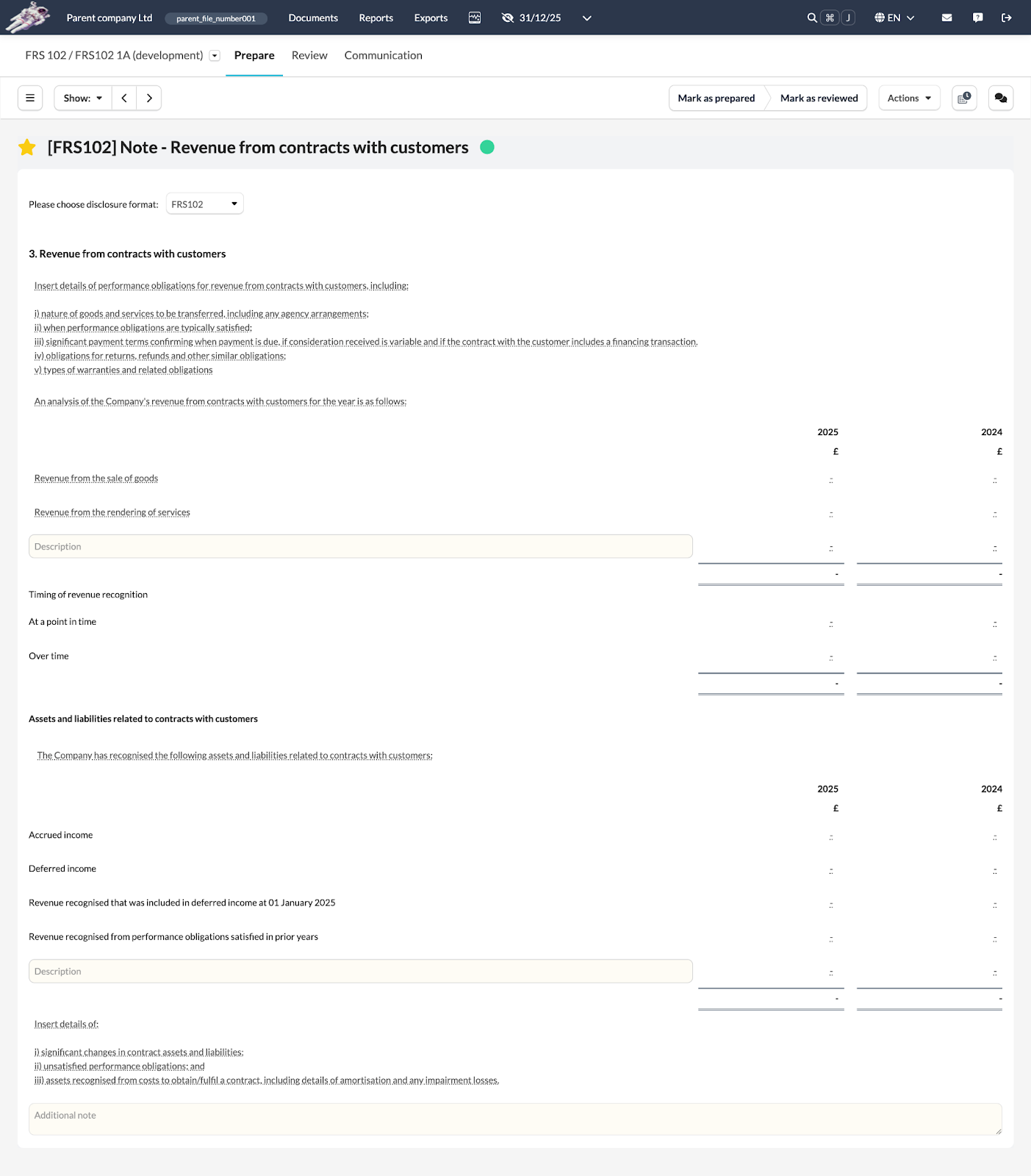

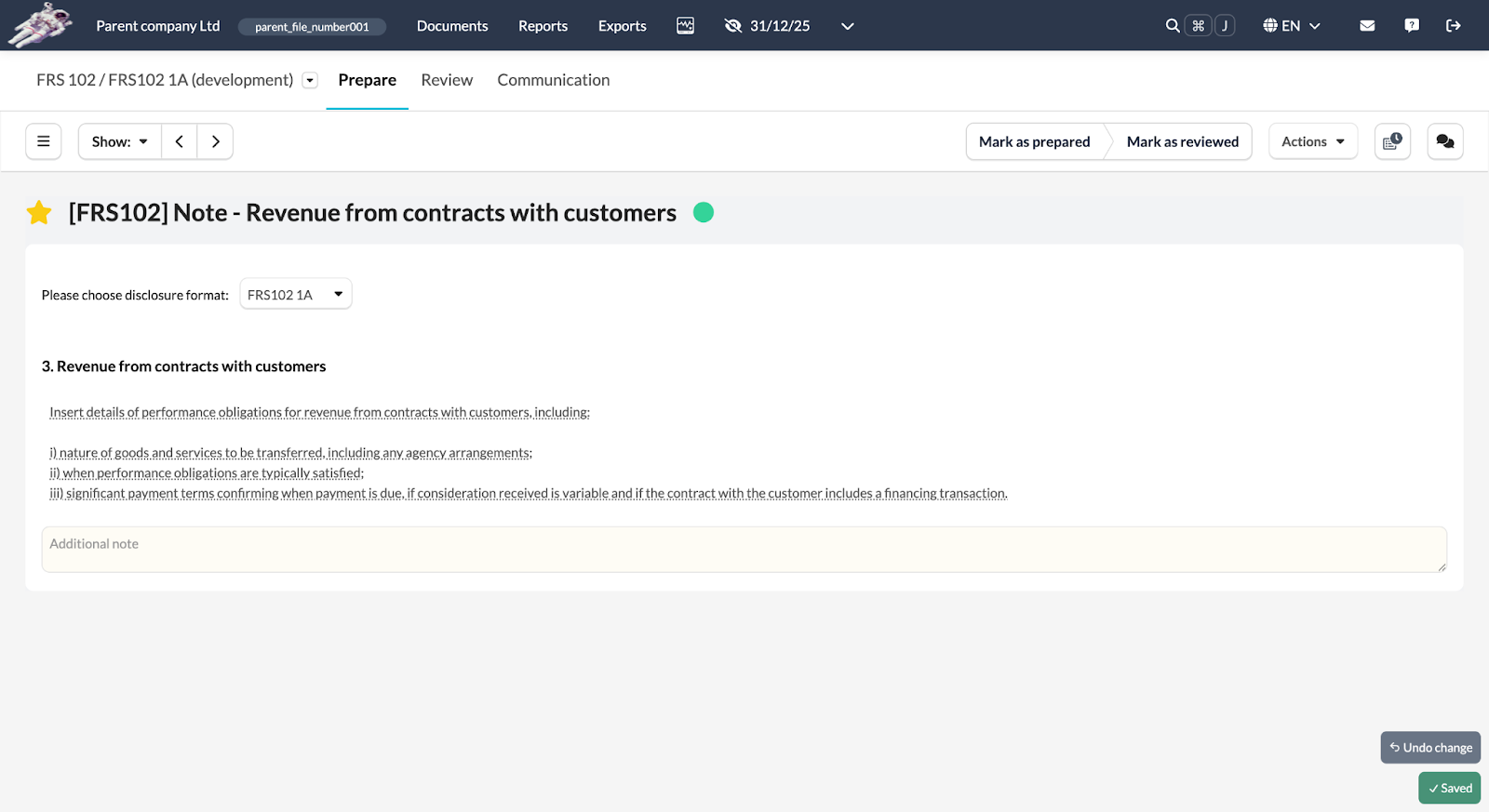

- Silverfin Impact: You will need to look closely at bundled contracts (such as software sold with hardware) to see if the timing of revenue recognition needs to be split. To facilitate this, a new "Revenue from contracts with customers" accounts note has been added to Silverfin. For full FRS 102, this note provides all the necessary space for relevant quantitative and qualitative disclosures. For FRS 102 Section 1A, the note includes dedicated space to capture the details of performance obligations, ensuring that all entities meet the new transparency requirements.

FRS102:

FRS102 1A:

3. Going Concern: From "Encouraged" to "Mandatory" Disclosures

- The Change: For the first time, all companies, including those using Section 1A, must provide a specific note in their accounts explaining the basis on which they believe the company will continue to trade. You must explicitly state that management has looked ahead at least 12 months and disclose the significant judgements or assumptions made.

- Context: In a volatile economy, the FRC wants to ensure that small company accounts aren't silent on their survival. What was previously "suggested" is now a legal requirement to ensure the accounts provide a "true and fair view."

- Applicable Frameworks: This primarily impacts FRS 102 Section 1A, as these disclosures were already standard practice for full FRS 102.

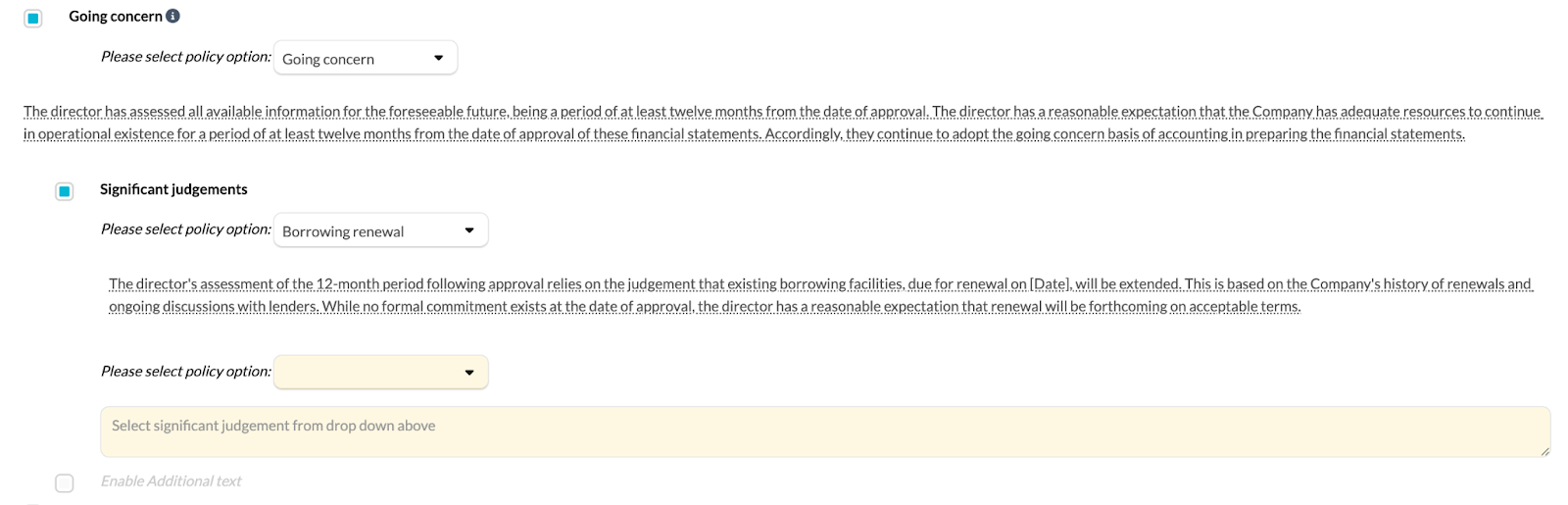

- Silverfin Impact: The Going Concern section of the accounting policies note has been redesigned to accommodate these mandatory requirements. New drop-down menus allow you to select the overall going concern status and choose from a list of significant judgements. Additional text boxes are also available for you to provide extra custom wording where specific detail is required.

4. Supplier Finance Arrangements: The "Early" Change (1 Jan 2025)

- The Change: If a company uses "reverse factoring" or third-party finance to pay its suppliers, it must now clearly disclose these arrangements and the amount of debt involved.

- Context: These schemes can make a company's cash flow look healthier than it is by hiding bank debt within "trade payables." This new rule brings these arrangements into the light so users can understand the company's true liquidity.

- Applicable Frameworks: This applies to FRS 102 and FRS 102 Section 1A. It does not currently apply to FRS 105.

- Silverfin Impact: You must disclose the total amount of liabilities sitting within these schemes and the typical payment terms. Note that this takes effect for periods starting 1 January 2025. To facilitate this, a new checkbox has been added to the bottom of the "Creditors: amounts falling due within one year" note. Enabling this checkbox allows you to separate out the necessary disclosure and provides dedicated input fields to record the specific terms of the arrangement.

5. Section 1A "Small Entities": New Mandatory Disclosures

- The Change: The "reduced disclosure" era for small companies is ending. You are now required to provide more detailed notes on areas like share-based payments, deferred tax, and dividends.

- Context: The FRC found that many small company accounts were too brief to be useful. By making these notes mandatory, they are raising the standard of reporting to ensure small company accounts are genuinely "true and fair."

- Applicable Frameworks: This section applies exclusively to FRS 102 Section 1A.

- Silverfin Impact:To ensure compliance with the new standard, Silverfin includes relevant disclosures as default requirements, removing the need for the user to override and include. Including but not limited to:

- Share-Based Payments: You must now provide details on any arrangements including the relevant profit and loss charges and liability values.

- Deferred Tax: A full breakdown of the deferred tax balance is now required.

- Dividends: You must disclose dividends declared and paid during the period for each share type.

- Related Parties: More transparency is required for transactions with anyone closely linked to the business.